More Problems in UK Property Ownership Expected 2022 to 2023

The years from 2019 to 2022 have been some of the most chaotic years in modern history. Many people have suffered and lost financially from the economic disruption caused by a cascading series of global disasters. However, there is also truth in the saying that what is a crisis for some is an opportunity for others.

Do you feel you are in a housing boom? According to HM Revenue and Customs data, residential transactions were up 36% over the previous year, and property solicitors and conveyancers conducted over 100,000 transactions each month. Ever since the start of 2021, the property market went into overdrive.

Part of the reason why there was a surge in housing purchases during the heavy Covid years was that with a lack of an easy outlet for discretionary spending, many people have managed to build up their savings. Unemployment and furlough assistance schemes of the government, along with rent and mortgage relief subsidies, and their experiences through lockdown, lead many people to deeply reprioritize the value of ownership vs renting. It was a confusing time, but property solicitors were on hand to help prospective new owners claim as much government aid and reimbursement as they could reach.

The market approaching 2023 may seem to be cooling, however. As a consequence of this spending and the ending of government assistance, housing prices are spiking fast and hard.

As written in The Times:

In May 2020, the Bank of England feared that property prices would fall because of the pandemic, but in fact, the sector not only survived but thrived. In January 2022, the average house price jumped to £276,759 which is a record high.

Tarrant Parsons, senior economist for the Royal Institution of Chartered Surveyors (RICS) stated:

“It is little surprise that housing market activity is now losing some momentum. With monetary policy set to be tightened further over the coming months, sales expectations point to a further softening in transaction volumes going forward.”

High prices lead to a less enthusiastic market that mainly benefits those who are already property holders. With homes moving out of reach, rental properties are also increasing to take advantage of their positioning.

Is it too late to join the property rush?

Should you still try to buy or continue renting?

How did the government address the coronavirus housing crisis?

In a report by the BBC at the tail end of 2019, the National Housing Federation estimated that just in England alone, 8.4 million people lived in unaffordable or unsuitable accommodation, of these 3.6 million living in overcrowded homes and 1.4 million in poor quality homes. An estimated 2.5 million lived in “hidden households” that they cannot afford to move out of; this includes house shares, live-in workers, caregivers and adults living with their parents, or people living with a partner or ex-partner. Over 400,000 people were already homeless or at risk of homelessness.

Issues such as overcrowded housing and inability to afford their rent or mortgage were endemic.

The housing crisis is founded on the mismatch of supply and demand. Even with the increasing number of households, fewer homes are being built. Public funding dried up drastically, expecting the private sector to pick up the slack, a hope which failed to materialize.

COVID-19 mandating indoor separation and social distancing was in some way a vital shock to the system.

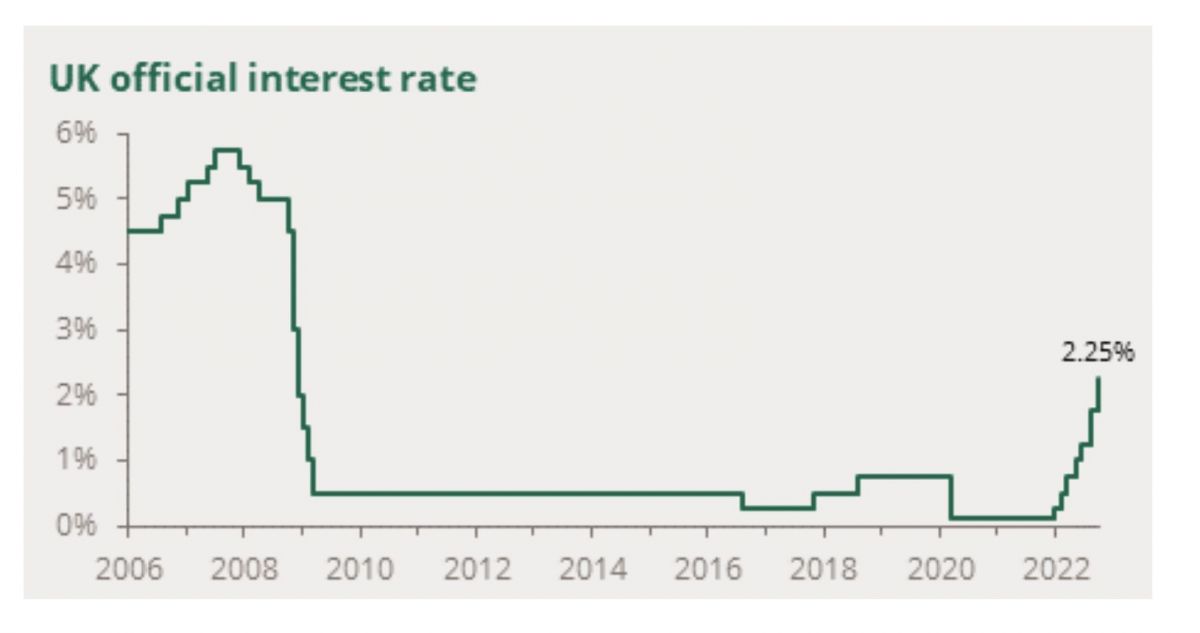

Lowered cost of debt

While lowered interest rates are terrible for savings, these conditions are primed for people who want to take on loans fuel their home ownership and businesses. In March 2020, the Bank of England’s Monetary Policy Committee (MPC) dropped interest rates down to 0.1% the lowest they have ever been.

This was the situation until December 2021. Since, the MPC had been increasing rates steadily until they are now at 2.25%, significantly higher than the pre-Covid years. This is said to be in response to rising inflation.

Tax Holiday on property purchases

Homebuyers in England gained a £6.4 billion tax break from the Covid Stamp Duty holiday. While this represents a loss of income to the treasury, an increase in transactions over the 15 months only expressed itself as a £1 billion reduction compared to the equivalent pre-pandemic period in 2018 to 2019.

The Stamp Duty Land Tax applies to properties over £250,000. It is paid in tiers, such as:

| Property or lease premium or transfer value | SDLT rate |

|---|---|

| Up to £250,000 | Zero |

| From £250,001 to £925,000 | 5% |

| From £925,001 to £1.5 million | 10% |

| Above £1.5 million | 12% |

The SLDT also applies to residential leasehold properties, such as flats.

You will have to pay additional rates on top of the standard SLDT rates if buying a residential property means you would own more than one.

The Stamp Duty Holiday meant that while in effect, homeowners had to pay none of this up to the first £500,000. Starting in July 20202, it was introduced as a way to re-ignite the property market. It did show a positive effect, with real estate agents reporting a boom in inquiries and 1.3 million buyers in England paying no stamp duties.

This ended on 30 June 2021.

Starting September 2021, the brackets mean:

| Property or lease premium or transfer value | SDLT rate |

|---|---|

| Up to £125,000 | Zero |

| From £125,001 to £250,000 | 2% |

| From £250,001 to £925,000 | 5% |

| From £925,001 to £1.5 million | 10% |

| Above £1.5 million | 12% |

For example, assuming the property you are buying is worth £650,000, you would pay

2% of 125,000 + 4% of 400,000 = £2,500 + £16,000 = £18,500

Which would make the total required loan amount at least £668,500. If this was a second property to a home or building you already owned, you may now have to pay 5% on top of the SLDT rates.

Essentially, treat the 0% tax bracket at 5%, the 2% at 7%, and the 5% as 10% and so on.

This would make the total SLDT due £55,000.

This may cool enthusiasm for property owners who wish to buy to let. There are proposals (see the Mini Budget below) to lift the minimum tax bracket back to £250,000.

The 95% Mortgage Guarantee Scheme will end

Otherwise known as the 5% deposit mortgage, this scheme allowed first-time buyers to borrow up to 95% of the value of their home. This was a strong enticement for both buyers and sellers.

Launched on April 2021, with it Housing Secretary Rt Hon Robert Jenrick MP said

“Together we can turn ‘Generation Rent’ into ‘Generation Buy’.”

For most lenders, the requirements are that

- The property will be a residential mortgage (i.e., the only home of the applicant)

- You apply for a repayment mortgage (i.e., pay off both capital and interest per month)

- Have a deposit of between 5% and 9.99% for a 95% Loan-to-Value mortgage

You can’t use the scheme to buy

- A new build property

- A second home

- A buy-to-let property

- An interest-only mortgage (I.e., pay only the interest per month and the capital in full at the end of the term)

Income requirements may vary, but normally the LTV mortgages range from 75% to 90%.

This scheme will end this 31 December 2022.

The upcoming No-Fault Eviction Ban

As part of the Renter’s Reform Bill, it will no longer be possible for private landlords to repossess properties from shorthold tenants without having to establish fault (Section 21 No-Fault Evictions). This is a welcome change for 11 million private renters in the country. For landlords, while Section 21 is abolished, Section 8 Grounds for Possession are strengthened.

This will take effect next year.

The Mini Budget is an unpredictable growth plan

The 2022 Mini Budget is called such because it is not a full Budget of the United Kingdom set by the HM Treasury for the following fiscal year. Also known as the “Growth Plan”, it is a proposal to boost economic growth through tax cuts, the necessary expenditures being paid for by increasing the National Debt. This will have drastic and far-reaching consequences if it comes into force in its present form.

The Mini Budget appears on the backdrop of a Cost of Living Crisis in the UK, impacted by many factors such as the continuing response to the pandemic, the 2022 Russian invasion of Ukraine, the exchange rate of currency, a rapid increase in inflation, and other global factors in flux.

Some of the proposals in the mini budget had already been withdrawn, and the rest are still uncertain. However, it is expected that some form of the mini budget will take effect next year.

Some expected key points in the mini-budget are:

- The basic income tax rate should be reduced from 20% to 19%.

- Withdrawn. The basic rate of income tax will remain at 20% indefinitely.

- Abolish the 45% additional rate of income tax for annual income over £150,000.

- Withdrawn. The 45% rate will be retained past April 2023.

- Reverse the temporary 1.25% rise in National Insurance contributions.

- Carries on as announced.

- Scrapping the introduction of the Health and Social Care Levy tax, which imposes the 1.25% increase permanently.

- Carries on as announced.

- Reverse the 1.25% increase in tax rates that apply to dividend income.

- Withdrawn. The rates that apply since April 2022 will remain beyond April 2023.

- Repeal the 2017 and 2021 reforms to the IR35 off-payroll working administrative rules

- Withdrawn. The 2017 and 2021 IR35 reforms will remain in place.

- Do not increase the rate of Corporation Tax as was scheduled to rise to 25% on April 2023.

- Withdrawn. The main rate of corporation tax will increase from 19% to 25% as previously planned.

- Maintain the rate of tax-free Annual Investment Allowance (AIA) instead of being reduced to £200,000.

- Carries on. The AIA indefinitely remains the same.

- Extended the Seed Enterprise Investment Scheme (SEIS) to by 2/3 more access to £250,000 of SEIS investment by start-up companies, and for the maximum amount that can be invested by individual investors to be doubled to £200,000.

- Carries on as announced.

- Increase the value of Company Shares options that workers can obtain to £60,000, a doubling of the previous limit.

- Carries on as announced.

- Increase the no-tax band for the Stamp Duty Land Tax (SDLT) to the first £250,000 payable.

- Carries on as announced and takes effect immediately.

- Increase the threshold that first-time buyers begin to pay SDLT on residential property from £300,000 to £425,000, and the maximum value of a property on which first-time buyers’ relief can be claimed, from £500,000 to £625,000.

- Carries on as announced and takes effect immediately.

- Add a new VAT-free shopping scheme for non-UK visitors to Great Britain.

- Withdrawn. This will not be implemented.

- Freeze Alcohol Duty rates for 1 year instead of increasing.

- Withdrawn. This will not be implemented.

- New Investment Zones in England

- Status unknown.

- Scrap the maximum cap on banker’s bonuses.

- Status unknown.

- Two-year cap on energy bills up to £2, 500 and freeze wholesale gas and energy prices for businesses

- Unknown, but may continue.

- The closure of the Office of Tax Simplification

- Will take effect once the next Finance Bill receives Royal Assent.

The mini budget has many critics, including even the IMF. It does have some immediate benefits especially for property owners with the reduction in SDLT taxes. Energy rate caps help property owners. Pensioners hoped to benefit from the reduction of taxes on dividend income.

The announcement had already almost immediately caused a fall in the value of the sterling (vs the dollar and other major currencies) and gilts (bonds issued by the UK government) causing the Bank of England to buy back up to £65 billion in gilts to secure the stability of pension funds.

The mini budget is a complex and contested event, and we must watch out for how it develops. While it remains undecided, the market trends toward volatility and high prices to entry.

What are your options in 2023?

If you would ask property solicitors if you should enter the market, the main question is “for what purpose?” If you would like to possess a home, then almost universally the response is that “the best time to begin is as soon as possible”.

There is zero incentive for rentals to ever lower prices. Once a rate has been set, it can only ever increase for the next tenant. However, we should be too quick to assign malice to landlords – if conditions were too uneconomical to cause landlords to exit the sector, this could also reduce access to housing for those who cannot afford to buy and those who are unable to access social rented housing.

The upcoming year is expected to be much more welcoming for first-time home buyers than those who wish to pursue a more flexible mortgage with a buy-to-let plan.

However, every crisis is an opportunity.

Do not try to DIY this. Contact a lease extension property solicitor to assess your options, and this might be your best chance to find the silver lining. The one who acts soonest loses out the least.